Read through planning documents across North America and you're bound to find language that refers to low-rise residential neighbourhoods as "physically stable areas" where the "existing neighbourhood character" is paramount. But to be more precise, what this kind of language is actually saying is not that these neighbourhoods need to be broadly stable; it is saying that they just need to look more or less stable.

Here in Toronto, for example, it has been widely documented that many of our low-rise neighbourhoods are losing people. Household sizes are getting smaller, and houses that used to be subdivided are being returned to single-family use. A similar thing is happening in other cities like New York:

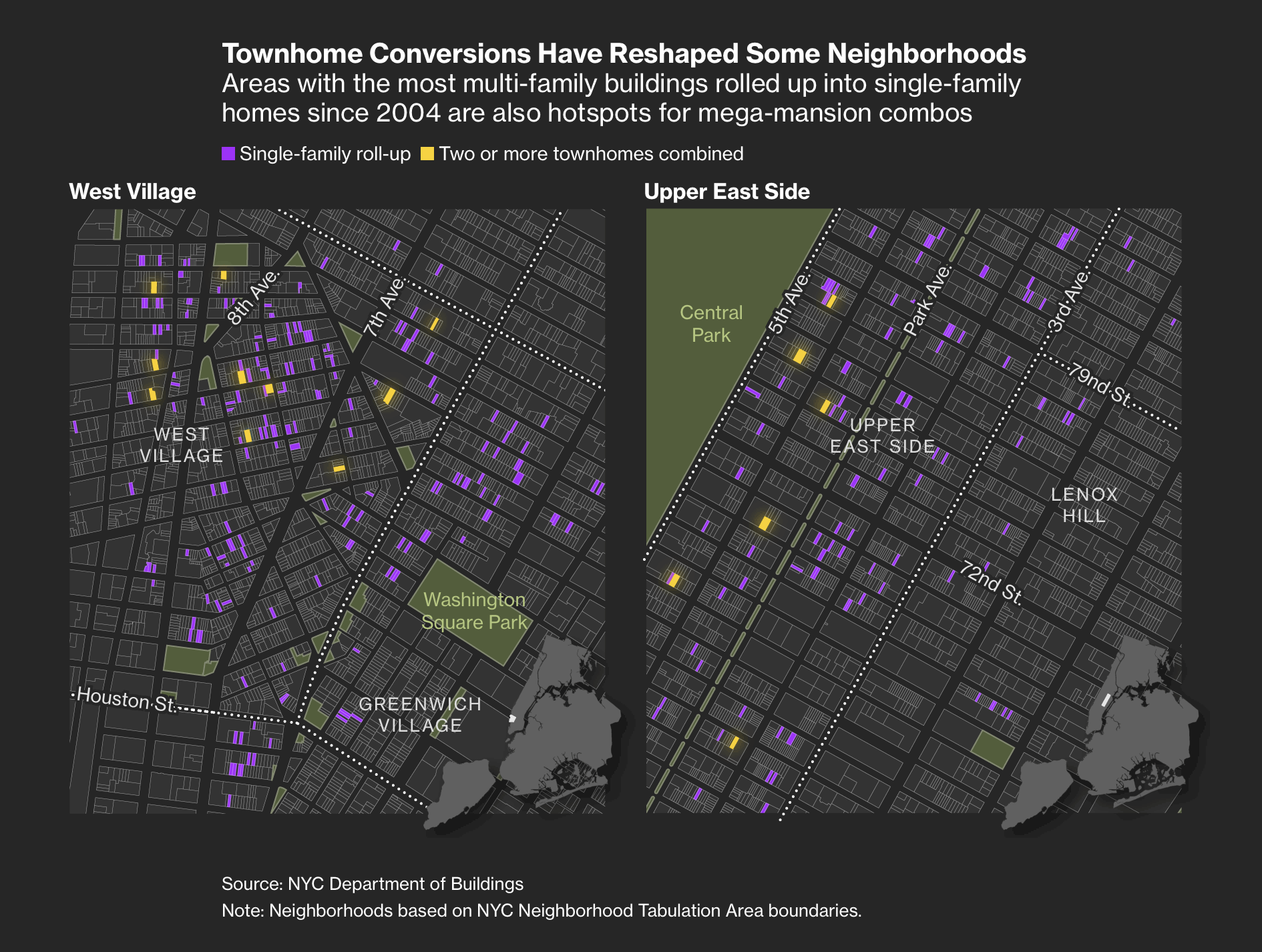

Bloomberg News recently reported that since 2004, at least 9,300 homes have been lost as a result of multi-family buildings getting "rolled up" into single-family homes. More recently, the city has even seen an increase in people combining two or more buildings into large urban mansions.

And while the total number of homes removed is relatively small for New York as a whole, it can be quite impactful to individual neighbourhoods. In the West Village, where there's a high concentration of rowhomes and townhouses, Bloomberg estimates that one out of every six small apartment buildings has been rolled up into a single-family home since 2004!

From a built form standpoint, you could say these are "physically stable" areas that are obediently adhering to their existing neighbourhood character. But under the hood and behind their street walls, they are clearly changing.

It is one of the great ironies of city building. People often fear new development because they worry it might disrupt the character of a neighbourhood. But preventing development does not guarantee stasis. In fact, we know that not building new housing actually increases the pressures felt on a city's existing housing stock, as people compete for a more fixed amount of supply.

The wealthy can always outbid the less wealthy on housing. So if you don't provide any new options, the wealthy will just buy up the existing stuff and turn it into what they want. Alternatively, you can build more housing and create a "moving chain" that frees up more existing housing for people of lower incomes.

It's not easy gaining support for pedestrian-only streets. Here in Toronto, Kensington Market is a neighbourhood that has been under consideration for pedestrianization for as long as I can remember. Yet it remains an aspiration, largely because of a number of common objections: it will hurt local businesses, lower foot traffic, and limit access for those with mobility issues.

Yonge Street in downtown Toronto went through a similar debate, and the end result is a plan that will prioritize pedestrians, while still allowing one vehicle lane in each direction. This will still be a nice improvement, and my understanding is that the option to fully pedestrianize has been or will be designed in. Construction is expected to start on this in 2030, once the Ontario Line Queen subway station is complete.

But there are cities that are going all the way. This week, it was announced that London has approved the pedestrianization of Oxford Street, specifically the stretch between Orchard Street in the west and Great Portland Street in the east.

Oxford Street is one of the most important thoroughfares in the world, and one of, if not the, busiest shopping streets in Europe. It is estimated that nearly 500,000 people visit it each day, meaning that most are not travelling there by car.

Pedestrianizing Oxford is an idea that arguably dates back to the 1960s, when a plan was put forward to create pedestrian-only walkways on top of podiums; although, this may have been more about getting people out of the way of cars. Pedestrianizing the street was also a prominent part of Mayor Sadiq Khan's platform when he was first elected in 2016, some 10 years ago. So, it too has had its opponents.

However, consultations done last year showed that nearly two-thirds (63%) of Londoners were in favour of pedestrianizing the street — a figure that increased to almost three-quarters (72%) when the question was asked to people who had specifically visited the area within the last 12 months.

Data from similar pedestrianization projects completed around the world indicates that both foot traffic and retail sales should increase once the project is built out. And I have little doubt that the same will prove true here in London. If you can't pedestrianize a pre-eminent, transit-rich street in one of the world's capital cities, then where can you?

This is an interesting chart from the Globe and Mail. It shows GDP, Gross Domestic Savings (how much a country's residents and businesses save), Gross Fixed Capital Formation (technical term for investments in productive long-term assets), and the share of total investment going into housing for the 20 largest economies in the world.

One of the key takeaways from the chart is that Canada invests the most into residential real estate (figures are from 2024). Now, I'm not an economist, but the risk here is that we are tying up too much of our capital in housing, as opposed to investing in new ideas, emerging tech, and the future. And this imbalance could help explain why Canada has had weak productivity growth for decades.

Housing demand should be a byproduct of a strong economy; simply building housing won't drive an economy forward on its own. And I say this as a developer of housing.

That is why the typical standard for most central banks is a target inflation rate of 2%. This leaves a factor of safety in case you miss your target. Because if you target 0% and end up with a negative number, then you're in trouble. A negative number is significantly worse than moderate inflation. The principal problem with deflation is that consumers start expecting goods and services to be cheaper next month and stop buying non-essential items, creating a vicious cycle with prices.

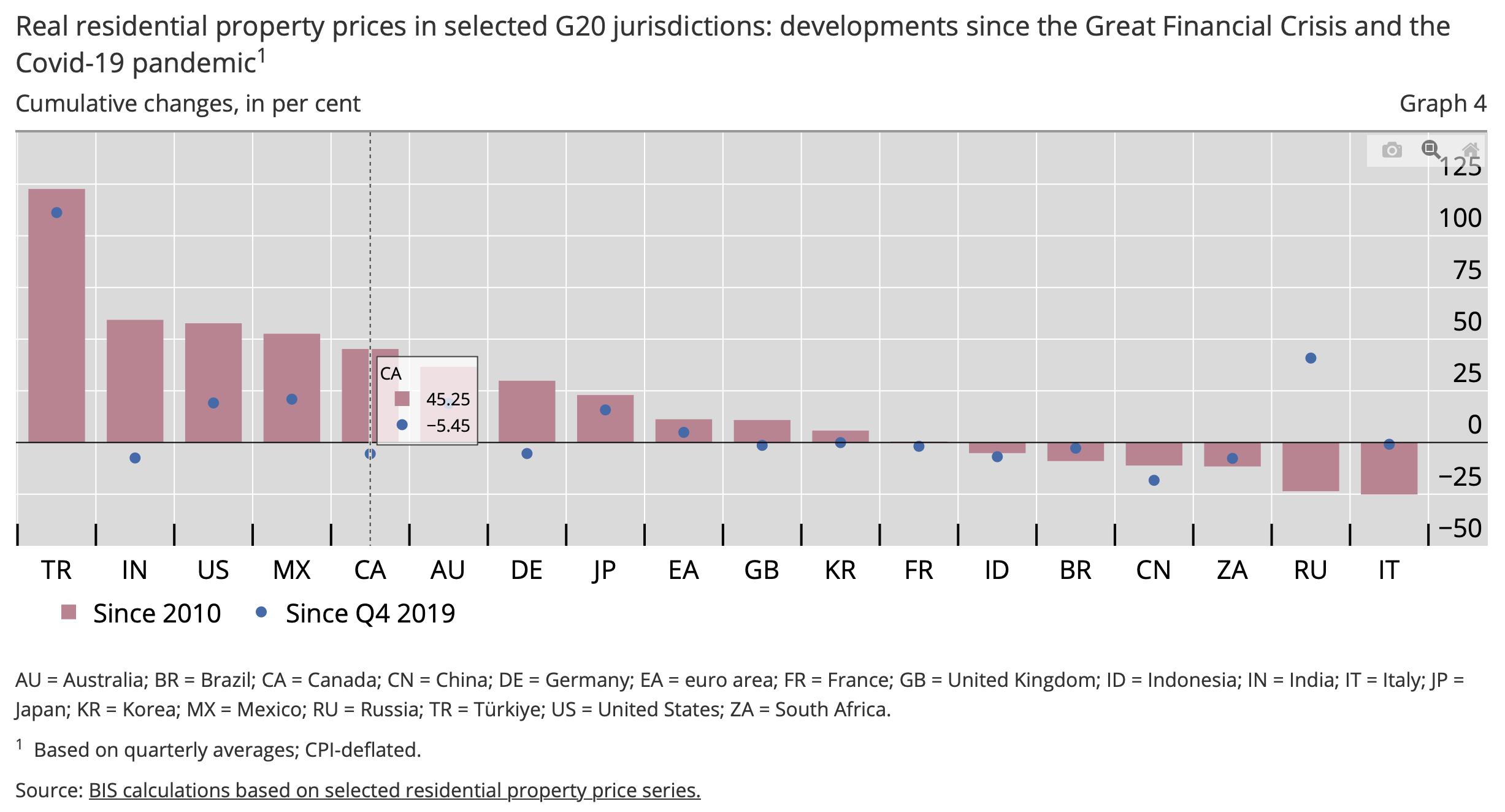

I think we are seeing this same psychology play out with real estate in Canada (though not in every local market). According to the above charts from the BIS, real residential property prices across Canada were down just over 5% year-over-year in Q3-2025. And since Q4-2019, they were cumulatively down 5.45% (but up ~45% since 2010 after the Great Financial Crisis). Right now, many buyers are waiting on the sidelines, just in case things get cheaper.

But I expect things to stabilize and feel better toward the end of 2026 and into 2027. And once that happens, a different buyer psychology will come to the fore.

Last month, we talked about how even "luxury" housing can improve overall housing affordability in a market. In that post, we spoke about a recent study that looked at the downstream effects of a new condominium tower in Honolulu. Today, let's look at Switzerland.

I stumbled upon this working paper on Twitter. The authors are Lukas Hauck and Frédéric Kluser, both from the University of Bern. In it, they look at the country-wide effects of new residential housing supply in Switzerland and, more specifically, the "moving chain" that new supply produces.

Moving chains work generally as follows:

A household moves into a newly constructed home

Their previous home becomes vacant

Another household moves into this vacant unit, leaving their previous home vacant

And the process continues, until someone breaks the chain (which can happen by way of a new household being formed or someone moving in from out of the market)

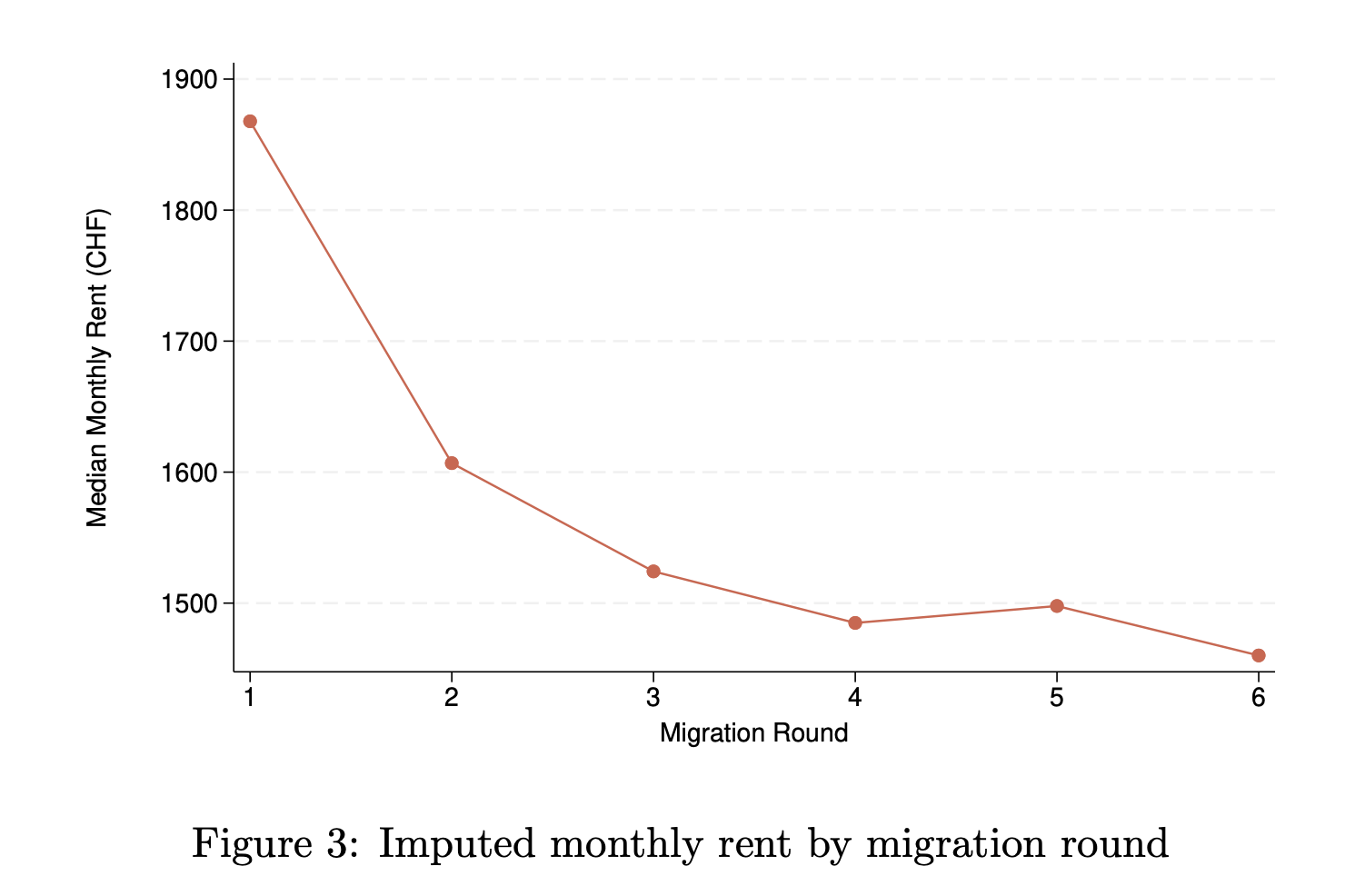

The authors found that these moving chains are relatively short in Switzerland. Approximately 75% of them terminate within three migration rounds. But this doesn't mean that these chains aren't critical for the market.

Importantly, they found that every new market-rate unit typically results in 0.75 moves for households with below-median incomes. So, that is 75 moves for every 100 new homes constructed.

The reason why new supply ends up also benefiting lower-income households is because there's a clear income and rent gradient across the moving chain:

New housing (migration round 1) is typically priced at the highest end of the market. This makes sense because we know that development happens on the margin. But by migration rounds 2 and 3, median rents fall off noticeably, creating housing opportunities for other people.

New market-rate housing is sometimes criticized for only serving one segment of the market. But once again, we see evidence that it helps to ease overall housing pressures. There are other indirect benefits that shouldn't be ignored.

Craving that next escape? This week's scoop: Insider scoops on offbeat spots, cultural dives, and savvy hacks to level up your travels – all from my real-deal journeys.

Dive into our newest post and let it spark your own epic plans.

What's your take? Favorite hidden gem? Dream destination wish list? Reply, comment, or share – your vibes keep this community buzzing!

Your cheers, likes, and shares fuel our globe-trotting tales – thanks for being part of the ride.

Keep wandering,

– The Knycx Journeying Team

Visit our website at Knycx Journeying for more exciting content.

Johannesburg's apartheid history through key sites like Soweto and Constitution Hill plus Cradle of Humankind. Tips for culture seekers in South Africa.Continue reading